Typical Accounting Terms and Definitions for Design/Builders and Remodelers

Early in my career as a remodeling business owner I struggled to learn about accounting and understand accounting principles. One big obstacle getting in the way for me was understanding the language of accounting. All too often I didn’t know the definition of terms seminar speakers and my accountant used when explaining things to me. Worse, sometimes I was assuming the wrong definition. What I came to realize was that I needed to learn the terms and the definitions if I really wanted to wrap my head around small business finances.

That learning experience and the difference it made for me sticks with me even today. For example, every time I start working with a new remodeler or design/builder as their business consultant or coach I make it a first priority to be sure my client knows the difference between margin and markup. Many a remodeler has made the mistake of figuring out the margin they need to cover overhead and profit only to assume they can then use that same number as the markup for establishing their project selling prices. When I explain the difference the light bulb goes off; shedding light as to why they are not achieving their required gross profit margin and therefore have no or even negative net profit.

That learning experience and the difference it made for me sticks with me even today. For example, every time I start working with a new remodeler or design/builder as their business consultant or coach I make it a first priority to be sure my client knows the difference between margin and markup. Many a remodeler has made the mistake of figuring out the margin they need to cover overhead and profit only to assume they can then use that same number as the markup for establishing their project selling prices. When I explain the difference the light bulb goes off; shedding light as to why they are not achieving their required gross profit margin and therefore have no or even negative net profit.

KEY BUSINESS CONCEPTS TO LEARN AND UNDERSTAND

- The total amount of money that can be collected during one business year for work completed by the company should be determined based on past experience and/or the capabilities of the company. (Volume)

- Gathering known business operation expense figures for the anticipated volume of installed sales, you can create an estimate for what it will actually cost you just to be in business even if you don’t produce any work. These are expenses that cannot be assigned to a particular project. (Overhead)

- By being honest with yourself, rewarding yourself for the risk of being in business, and by planning for the future growth of your business, your business can plan for financial compensation. (Profit)

- Overhead and Profit added together make up the total Indirect Costs of the business.

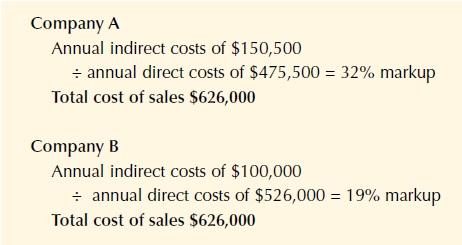

- By knowing your overhead and what you want for planned profit, you can determine how much you need to charge over and above the estimated project cost to be successful. (Mark-up) Markup is determined by dividing the total Indirect Costs by the total Direct Costs.

- Predicting the cost of labor, cost of project related equipment, as well as material and subcontractor costs, you can determine what the production related cost should be to complete the project. (Estimate)

- By increasing the estimated cost with a predetermined mark-up amount you can establish the price your company must charge to successfully complete a project. (Sell Price)

- By keeping track of actual production related expenses (Direct Job Costs), and comparing the expenses against the estimated project cost you can measure the success of your production performance as well as the accuracy of the estimate that was created. (Job Costing)

- Through the use of job costing you will know how much money is left from the sell price after paying all production related expenses. (Gross Profit) This is expressed as the Gross Profit Margin. (GPM) To calculate the Gross Profit Margin, divide the gross profit for a particular project (or time period) by the total sell price of that project (or time period).

- After paying all overhead related expenses, from the gross profit, you can determine how much money is left to compensate the business. (Net Profit)

- It is important to know how much business your company must complete in installed sales before it actually starts making a profit. (Break Even) This is determined by dividing the known total overhead expense by the gross profit margin.

Suggestion

As a suggestion, post this list somewhere near your desk so it’s in view at all times. Next time you’re reading a blog or magazine article that uses one or more of these terms you’ll be able to quickly find or verify their meaning. You’ll be amazed how quickly you can commit this information to memory if you do so.

Click here to download and print the list as a one page poster.

Markup on anything you sell needs to be based on projected overhead costs and net profit requirements for producing a specified volume of work. Be careful using someone else's markup suggestions particularly if they have not done the math to figure it out.

Markup on anything you sell needs to be based on projected overhead costs and net profit requirements for producing a specified volume of work. Be careful using someone else's markup suggestions particularly if they have not done the math to figure it out. Also, many magazine articles advise contractors to apply a “professional markup” to their bids. But what, exactly, is a professional markup? Does a 50% markup make you a professional, or should you apply 67% to qualify? The simple answer is, if you don’t know what markup your company needs to use, you’re not a professional, and therefore you’re not using a professional markup. But if you know the formulas for determining margin and markup, you have a working financial tool, rather than a magic number suggested by some remodeling guru or pulled out of a hat by another remodeler.

Also, many magazine articles advise contractors to apply a “professional markup” to their bids. But what, exactly, is a professional markup? Does a 50% markup make you a professional, or should you apply 67% to qualify? The simple answer is, if you don’t know what markup your company needs to use, you’re not a professional, and therefore you’re not using a professional markup. But if you know the formulas for determining margin and markup, you have a working financial tool, rather than a magic number suggested by some remodeling guru or pulled out of a hat by another remodeler.

Financial success doesn't happen by accident. Knowing your real costs can give you the confidence to estimate and sell at the right price.

Financial success doesn't happen by accident. Knowing your real costs can give you the confidence to estimate and sell at the right price.  Design/Build has caused a major role reversal. In most Design/Build situations, the contractor is now choosing the designer, after the project or design retainer has been sold! Finding a design professional who will work in this new role can be a challenge, but if the relationship is built for mutual benefit, all parties win, including the homeowner.

Design/Build has caused a major role reversal. In most Design/Build situations, the contractor is now choosing the designer, after the project or design retainer has been sold! Finding a design professional who will work in this new role can be a challenge, but if the relationship is built for mutual benefit, all parties win, including the homeowner.

Not all contractors or homeowners have creative design skills, but most can tell a good design from a bad one. A drive through your local area may provide a few good examples of projects where the contractor completed the design, but perhaps should have stuck just to the build part. The project could have met the client’s needs for space or function, but the end result may have been a T-1-11 box added onto a Victorian gem.

Not all contractors or homeowners have creative design skills, but most can tell a good design from a bad one. A drive through your local area may provide a few good examples of projects where the contractor completed the design, but perhaps should have stuck just to the build part. The project could have met the client’s needs for space or function, but the end result may have been a T-1-11 box added onto a Victorian gem.

Many expect Workers Compensation rates to increase significantly this year. The MA Workers Comp Rating and Inspection Bureau has recently applied for an average rate increase of 19.3%. According to the Insurance Journal, Commissioner Joseph Murphy will be holding a public meeting on March 30th on this request.

Many expect Workers Compensation rates to increase significantly this year. The MA Workers Comp Rating and Inspection Bureau has recently applied for an average rate increase of 19.3%. According to the Insurance Journal, Commissioner Joseph Murphy will be holding a public meeting on March 30th on this request.

While at JLC LIVE last week in Providence RI Many remodelers shared with me that they were seeing positive signs like increased leads and project budgets, and are now booking more work recently than they have experienced in the last several years. Having scaled back their staffing due to the recession they expressed concern about hiring production employees to meet the demand only to have to let them go if the demand softens. They were looking for solutions for their businesses that help keep good employees working full time. There are no guaranteed solutions. However with some planning and committing to some changes about how you do business, you can make it happen. Here is some of the advice I offered these attendees:

While at JLC LIVE last week in Providence RI Many remodelers shared with me that they were seeing positive signs like increased leads and project budgets, and are now booking more work recently than they have experienced in the last several years. Having scaled back their staffing due to the recession they expressed concern about hiring production employees to meet the demand only to have to let them go if the demand softens. They were looking for solutions for their businesses that help keep good employees working full time. There are no guaranteed solutions. However with some planning and committing to some changes about how you do business, you can make it happen. Here is some of the advice I offered these attendees: One thing I recommend is finding a real lead carpenter who can actually manage the job onsite with little interaction with the business owner after a proper hand-off of the project. For this to be successful the remodeler must look at what information needs to be collected and prepared before the hand-off from sales to production, conduct a successful hand-off, and actually empower and allow the lead carpenter to be a lead carpenter.

One thing I recommend is finding a real lead carpenter who can actually manage the job onsite with little interaction with the business owner after a proper hand-off of the project. For this to be successful the remodeler must look at what information needs to be collected and prepared before the hand-off from sales to production, conduct a successful hand-off, and actually empower and allow the lead carpenter to be a lead carpenter.  This change in business style is understandably difficult for someone who has in the past been in total control of everything in their business and has relied on micromanagement to get things done. Making the change requires new business practices and the changes can be fast-tracked with some mentoring/coaching to help the remodeler get through the structural and emotional adjustments required.

This change in business style is understandably difficult for someone who has in the past been in total control of everything in their business and has relied on micromanagement to get things done. Making the change requires new business practices and the changes can be fast-tracked with some mentoring/coaching to help the remodeler get through the structural and emotional adjustments required.

Paying the bills for yesterday’s project using the deposit money from a job you haven’t started yet may seem to solve the cash flow problem; however it only temporarily puts off the eventual reality that you are buying jobs instead of selling them. Due to the recession many contractors discovered this reality when the new job deposits dried up and there was no money in the bank to pay the bills for work already completed.

Paying the bills for yesterday’s project using the deposit money from a job you haven’t started yet may seem to solve the cash flow problem; however it only temporarily puts off the eventual reality that you are buying jobs instead of selling them. Due to the recession many contractors discovered this reality when the new job deposits dried up and there was no money in the bank to pay the bills for work already completed.

8 Smart Budget Curb Appeal Makeovers

8 Smart Budget Curb Appeal Makeovers 25 Manliest Homes in America

25 Manliest Homes in America Many contractors have asked me what volume of sales they should achieve before they implement the Lead Carpenter System. Like many other business decisions, it depends upon the reason you want to do it, but it also depends upon the company and the current condition of that company’s business systems. Without that information, answering the question based on assumptions could lead to disaster. Unless you and your company are properly prepared, failure of the Lead Carpenter System might be blamed on the system itself, rather than the business systems that are required to support it. The key is to adjust your business systems to support a true Lead Carpenter System, not adjust the lead Carpenter System to work within your existing business systems.

Many contractors have asked me what volume of sales they should achieve before they implement the Lead Carpenter System. Like many other business decisions, it depends upon the reason you want to do it, but it also depends upon the company and the current condition of that company’s business systems. Without that information, answering the question based on assumptions could lead to disaster. Unless you and your company are properly prepared, failure of the Lead Carpenter System might be blamed on the system itself, rather than the business systems that are required to support it. The key is to adjust your business systems to support a true Lead Carpenter System, not adjust the lead Carpenter System to work within your existing business systems. Get Your Support Systems Ready

Get Your Support Systems Ready

Many Design/Builders have found the Lead Carpenter System for production to be a very complimentary best practice when paired up with the Design/Build delivery system. When I owned my business it certainly proved to be the way to go for me and my employees.

Many Design/Builders have found the Lead Carpenter System for production to be a very complimentary best practice when paired up with the Design/Build delivery system. When I owned my business it certainly proved to be the way to go for me and my employees.  Create a written plan for implementation, including a realistic timeline.

Create a written plan for implementation, including a realistic timeline. Start implementing a piece at a time; assume it could take 1-2 years.

Start implementing a piece at a time; assume it could take 1-2 years.